PDP For Fleets - 3 Months Free

To enroll or not to enroll in a company-paid per diem program that includes a fleet per diem administration fee, that is the question.

Background: ABC is a truckload carrier that offers voluntary company-paid per diem. Drivers who enroll are paid $.045 CPM of which $0.10 CPM is allocated to per diem, less a $0.02 CPM fleet administration fee. Drivers who choose not to enroll earn a flat $0.45 CPM and can deduct per diem on their own tax return.

John Smith recently went to work for ABC and is unsure if he should enroll in the company per diem plan. He departs home every Monday morning and returns home Friday evening, averages 2250 miles per week and works 50 weeks a year. John is married, but his wife is not working. He owns a modest home, and pays state income, real estate and personal property taxes.

The motor carrier claims he will take home more money and pay less taxes if he enrolls in their per diem program even after giving back $2,250 in fleet administration fees.

Conclusion: John may save a few hundred dollars in federal taxes, but he must forfeit $2,250 of additional income to do so. In addition, the tax savings come at an additional cost: $9,000 of wages omitted from his Form W-2 that will be noticed by a home or auto lender and may lower his employer 401(k) match, social security and workers compensation benefits.

This article was written by D R Sullivan & Company, CPA PC, an accounting firm that has been providing taxpayer advocacy, consulting, and litigation services since 1998. The firm is tax counsel for Per Diem Plus, an automated per diem and expense tracking mobile app.

Please remember that everyone’s financial situation is different. This article does not give and is not intended to give specific accounting and/or tax advice. Please consult your own tax or accounting professional.

Copyright 2016 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.

First, and foremost, you want to make sure you have all expense receipts and documentation needed for any expenses you will be deducting on your tax return for 2016, especially major expense items like per diem and fuel. For your per diem expenses, be sure you have all 12 months of paper or electronic logs to substantiate time, date and place of the expense. Or, if you use Per Diem Plus®, all you need to do is run a report and send it to your accountant directly from the app. Unfortunately, per IRS Regulations, a calendar is not sufficient substantiation for per diem expenses.

If you are self-employed and have the ability to control when you invoice for end-of-year work, then delay invoicing for an end-of-year run until January, which will push the income into next year. This only makes sense if you expect to be in the same, or lower, tax bracket next year as this year.

If there are repairs that need to be made to your truck or supplies you need to purchase, etc. then make and pay for those purchases by year-end versus waiting until next year. Payment can be made using a credit card and still qualify for deduction in the current year even if you do not pay the credit card bill until next year.

Do you itemize your deductions rather than take the standard deduction? If so, then make some extra charitable contributions, cash or non-cash by the end of the year. However, be sure to obtain receipts for all charitable contributions regardless of the amount.

If you are on the borderline of being able to itemize, then aggregate deductions into one year or the other. This takes a little more planning. Examples include, paying an extra mortgage payment in one year to pay extra interest; paying two years of real estate taxes in one year, if you have control over the timing of payment (pay one on January 2nd to minimize interest and penalties and the other at the end of the year); and bunching charitable contributions into one year. Although the chance is slim, you do need to be cognizant of the Alternative Minimum Tax and whether this strategy could trigger it. You would want to discuss this with your tax professional before engaging in this strategy.

If you are self-employed, contributing to a retirement plan is a great way not only to save for retirement but to save taxes as well. There are several different plans to choose from. However, depending on which one you choose, governs when it needs to be set up. A SIMPLE plan would need to be set by October 31st of the first year of contributions; others need to be set up by December 31st. A SEP plan can be set up all the way up to the due date of the tax return, including extensions. Therefore, if you want to make a contribution but do not have the money by April 15th, you can extend your return in order to buy more time to make the contribution. Just remember, an extension to file the return is not an extension of time to pay the tax, just the SEP contribution.

IRA contributions must be made by April 15th even if you have filed for an extension. Generally, you can make a larger contribution to a plan other than an IRA, unless you plan to use the spousal IRA rules in order to double your contribution. This is another area where consulting with your tax professional may be beneficial to determine the best course of action.

Want to join the conversation? Drop us a line at info@perdiemplus.com

This article was written by Donna R. Sullivan, CPA of Per Diem Plus, LLC. Sullivan has over 25 years of tax consulting and preparation experience.

Please remember that everyone’s tax and financial situations are different. This article does not give and is not intended to give specific accounting and/or tax advice. Please consult your own tax or accounting professional.

Copyright 2016 Per Diem Plus, LLC. Per Diem Plus® proprietary software is the trademark of Per Diem Plus, LLC.

A Catch 22 For Drivers

Drivers currently retain ownership of their paper logbooks to comply with the IRS income tax regulations. Now that the U.S. Court of Appeals for the Seventh Circuit has upheld the ELD mandate and ruled that the FMCSA has satisfied the objections made by the Owner Operators Independent Drivers Association, who will “own” the logbook data1? While the media is awash with articles either applauding or deriding the court's decision, everyone has overlooked the mandate’s impact on tax compliance recordkeeping obligations for individual truck drivers. Everyone but Per Diem Plus.

The history of the IRS is that they ONLY accept driver DOT logbooks as proof of overnight truck driving trips to substantiate travel expenses, like per diem. Treasury Regulation 1.274-5A(c)(2) governs the rules for substantiation of travel expenses. A logbooks meets the requirements because it is a contemporaneous record that is created "at or near the time the expense or travel occurred"2 and establishes the "time, date and place" of the travel3. Contrary to popular belief a calendar or bookkeeper’s guesstimate worksheet of per diem trips does not fulfill these statutory requirements.

A Statutory Conflict - 6 month / 3 year rules

FMCSA Part 395 section 395.8(k)(1) requires motor carriers to retain all supporting documents used by the motor carrier to verify the information recorded on the driver’s record of duty status for a period of 6 months4. But...

Internal Revenue Code section 6501(a) establishes the statute of limitations for the IRS to assess taxes on a taxpayer expires three (3) years from the due date of the return or the date on which it was filed, whichever is later.

Drivers currently retain their logbooks to comply with income tax reporting and filing obligations. However, in my experience, since motor carriers own the ELD device they will assert ownership of the ELD data as well. And while fleets retain certain records required by FMCSA to comply with tax regulations, those using ELD’s promptly discard driver logbooks after 6 months. More troublesome is the revelation that many large fleets who were early adopters of ELD’s are now refusing to provide copies of the e-logs to their drivers. Will this behavior permeate the industry as fleets transition from paper to electronic logs?

What this means to you is that you may not have access to ELD data that is critical to both accurately claiming per diem expenses and defending yourself in the event of an audit. This will be particularly true if a driver is employed by multiple fleets during a calendar year. In the end, drivers will find themselves in a Catch 22 - a driver can have only one logbook that the motor carrier will now own so a driver cannot properly file income tax returns as they no longer have access to the logbook data.

Drivers that use Per Diem Plus have access to their data for four years whether they are driving for a company or themselves. Own your data and simplify your life by using the Per Diem Plus mobile app.

Want to join the conversation? Drop us a line at info@perdiemplus.com

This article was written by Mark W. Sullivan of D R Sullivan & Company, CPA PC, an accounting firm that has been providing taxpayer advocacy, consulting, and litigation services since 1998. The firm has nearly a decade of experience advising motor carriers and telematics providers on IRS substantiated per diem and is tax counsel for Per Diem Plus®, an IRS-compliant automated per diem and expense tracking Android and iOS app.

Please remember that everyone’s financial situation is different. This article does not give and is not intended to give specific accounting and/or tax advice. Please consult your own tax or accounting professional.

Copyright 2016 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.

FMCSA Part 395 section 395.8(k)(1)

Supporting documents are the records of the motor carrier which are maintained in the ordinary course of business and used by the motor carrier to verify the information recorded on the driver’s record of duty status. Examples are: bills of lading, carrier pros, freight bills, dispatch records, electronic mobile communication/tracking records, gate record receipts, weight/scale tickets, fuel receipts, fuel billing statements, toll receipts, toll billing statements, port of entry receipts, cash advance receipts, delivery receipts, lumper receipts, interchange and inspection reports, lessor settlement sheets, over/short and damage reports, agricultural inspection reports, driver and vehicle examination reports, crash reports, telephone billing statements, credit card receipts, border crossing reports, custom declarations, traffic citations, and overweight/oversize permits and traffic citations. Supporting documents may include other documents which the motor carrier maintains and can be used to verify information on the driver’s records of duty status. If these records are maintained at locations other than the principal place of business but are not used by the motor carrier for verification purposes, they must be forwarded to the principal place of business upon a request by an authorized representative of the Federal Highway Administration (FHWA) or State official within 2 business days.

![]()

The Per Diem Plus show truck, affectionately known as “Truck 4.04,” headed to the Great American Trucking Show in Dallas, TX. The show exceeded our expectations as we debuted our Apple iOS platform and educated drivers and fleet operators on how Per Diem Plus® takes the guesswork out tax-related record keeping.

The Per Diem Plus show truck, affectionately known as “Truck 4.04,” headed to the Great American Trucking Show in Dallas, TX. The show exceeded our expectations as we debuted our Apple iOS platform and educated drivers and fleet operators on how Per Diem Plus® takes the guesswork out tax-related record keeping.

“DON’T WAIT TO GET THE MOBILE APP EVERYONE IN THE TRUCKING INDUSTRY IS TALKING ABOUT” , Dave Nemo

According to Dave Nemo, per diem is one of the most common issues raised during his tax-talk call-in segment. Our tax experts, Donna and Mark Sullivan, sat down with Dave (Sirius/XM Road Dog Radio) to discuss how Per Diem Plus automates per diem tracking for drivers on paper or electronic logs and expense accounting and reporting.

GATS provided us a great opportunity to teach owner operators and company drivers, fleet operators and even Dave Nemo how easy PDP is to use. We had hundreds of attendees visit with us and learn about our 30-day FREE trial subscription with no credit card required.

Kellie, a veteran driver with Crete Carrier Corp, was the lucky winner in our YETI cooler.

Download Per Diem Plus today!

Copyright 2016 Per Diem Plus, LLC

Per Diem Plus®, a proprietary software application, which provides automatic per diem and expense tracking to truckers.

Per diem simply means a “per day” travel expense allowance. Although taxpayers have the option of keeping actual records of their travel expenses, the IRS has provided per diem allowances under which the amount of away-from-home meals and incidental expenses may be deemed to be substantiated. These per diem allowances eliminate the need for proving actual costs. However, a taxpayer must substantiate the amount, time, place and business purpose of expenses paid or incurred by adequate records or other evidence when traveling away from home1.

Both self-employed and employee truck drivers subject to the hours of services limitations of the Department of Transportation (DOT) can claim $63 for meals & incidental expenses (M&IE) for travel with the United States ($68 in Canada) and are not required to retain receipts or sales slips for these expenses. A trucker can deduct 80% of these expenses on their income tax returns2.

A truck driver who is away from home for only a portion of a day can prorate the M&IE allowance. For example, Per Diem Plus allows 75% of the M&IE rate where a driver departs their tax home after noon or returns home from a trip before noon.

No. Incidental expenses include only fees and tips given to porters, baggage carriers, hotel staff and staff on ships. Transportation between place of lodging and place where meals are taken and the mailing cost of filing expense reports are no longer included in the definition of incidental expenses3. Drivers using per diem rates may separately deduct expenses for postage, showers and reserved parking fees.

In order to claim any deduction, a taxpayer must be able to prove, if a tax return is audited, that the expenses were in fact paid or incurred. The IRS deems travel expenses particularly susceptible to abuse and requires truck drivers maintain an adequate accounting and sufficient documentary evidence to prove overnight travel. For example, logbooks, expense diaries or an IRS-approved software tool like Per Diem Plus.

Self-employed and employee drivers cannot claim per diem for lodging and are required to maintain documentary evidence for all lodging expenses4.

No. An individual is not away from home unless their duties require them to be away from the general area of their home for a period substantially longer than an ordinary workday and it is reasonable for them to need to sleep or rest5. For example, drivers who start and end a trip at home within the DOT 14 consecutive-hour “driving window” cannot claim per diem.

Tax home defined: An individual’s tax home is considered to be: (1) the taxpayer’s regular place of business, or (2) the taxpayer’s home in a real and substantial sense6. A taxpayer who is itinerant or someone who has a home wherever they happen to be working is never away from home for purposes of deducting traveling expenses.

This article was written by D R Sullivan & Company, CPA PC, an accounting firm that has been providing taxpayer advocacy, consulting, and litigation services since 1998. The firm has nearly a decade of experience advising large fleets and telematics providers on IRS substantiated per diem and is tax counsel for Per Diem Plus, an automated per diem and expense tracking Android app.

Please remember that everyone’s financial situation is different. This article does not give and is not intended to give specific accounting and/or tax advice. Please consult your own tax or accounting professional.

Copyright 2016 Per Diem Plus, LLC. The Per Diem Plus logo and Per Diem Plus are trademarks of Per Diem Plus, LLC.

(Revised July 2023)

Do home loan lenders understand how trucker per diem works, that is the question.

Background: An employee truck driver was recently denied a zero-down VA home loan. The reasoning? Because he received tax-free, company-paid per diem that was not reported as wages on Form W-2 and his income was too low for the VA loan. But if he did not receive per diem for two years they could use his wage statements as pure income. The loan officer’s position was,“You received it, therefore you spent it. So it's not available as part of your income."

I cannot help but wonder if this loan officer has ever actually prepared or even filed a U.S. individual income tax return. It is obvious he/she knows nothing about U.S. income taxes let alone how taxable income is computed.

Loan Officer Education - Taxes 101: Most taxpayers claims the standard deduction on their income tax return. The standard deduction is subtracted from adjusted gross income to calculate taxable income. The taxes owed to Uncle Sam are calculated from this figure.

Conclusion: The home loan lender clearly does not know that taxable income is always lower than adjusted gross income as a function of the Form 1040.

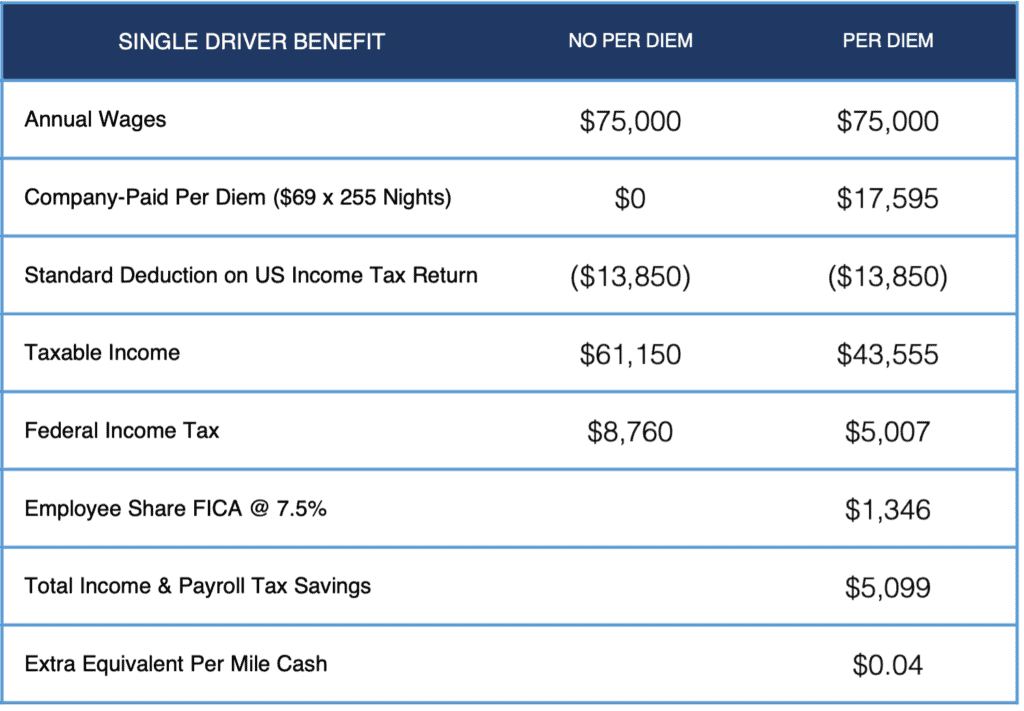

Discussion: For the sake of argument let us assume the driver participated in a company-paid per diem program that was reported in Box 12 of the Form W-2. Would the loan officer be correct? Maybe. In the below example the driver’s Form W-2 would show income of $43,555, which is $17,595 less than what would be reported if he did not receive company-paid per diem and will likely be noticed by a lender.

What the lender does not realize is the unique treatment of trucker per diem in the transportation industry. Per diem is first recorded as a pre-tax deduction; income and payroll taxes are deducted, and per diem is added back to the drivers settlement as a non-taxable reimbursement. The driver receives neither more or less money - per diem simply serves to lower the income and employment taxes and raises their tax home pay.

In the below table per diem saves a single driver about $5,099 in taxes, which equates to $99 extra tax-free cash to the driver (based 51 week).

PDP Small Fleets requires users to complete the account setup HERE before using the app.

Mark is tax counsel for Per Diem Plus. With nearly two decades of experience advising trucking companies on per diem issues, Mark was responsible for defining the Per Diem Plus software logic rules that automatically calculates trucker per diem in accordance with IRS regulations. He also previously served as the consulting per diem tax expert for Omnitracs.

In addition to his time working with Per Diem Plus, Mark works in private practice as an Enrolled Agent at Mark Sullivan Consulting, PLLC specializing in federal tax controversy representation and consulting. He also served as the consulting and expert witness for the Federal Defenders Office and private defense counsel in financial crimes cases in multiple federal district courts. Contact Mark W. Sullivan, EA

Disclaimer: This article is for information purposes only and cannot be cited as precedent or relied upon in a tax dispute before the IRS.

Copyright 2016-2023 Mark Sullivan Consulting, PLLC; Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.®

An employee truck driver asked the following question to the Per Diem Plus tax experts during the 2016 MidAmerica Truck Show: "Is cent per mile or IRS daily rate per diem better for a driver?"

The cent per mile per diem method has been the transportation industry standard for decades and is most often utilized by fleets who offer employee drivers company paid per diem. Under the cent per mile method a driver is paid only for miles driven and not nights away from home.

Although, a driver may travel 500 miles one day but only 250 miles the next, the distance traveled does not affect the need to eat three meals a day. To remedy this problem the IRS introduced the Special Transportation Industry* daily rate per diem that ignores miles traveled and relies on days away from home. The most beneficial aspect to a driver is that per diem can be claimed during a 34 hour restart and unforeseen delays like breakdowns, waiting for permits or weather.

The table below illustrates the advantage of choosing daily rate per diem:

This article was written by D R Sullivan & Company, CPA PC, an accounting firm that has been providing taxpayer advocacy, consulting, and litigation services since 1998. The firm has nearly a decade of experience advising large fleets and telematics providers on IRS substantiated per diem and is tax counsel for Per Diem Plus, an automated per diem and expense tracking Android app.

Please remember that everyone’s financial situation is different. This article does not give and is not intended to give specific accounting and/or tax advice. Please consult your own tax or accounting professional.

Copyright 2016 Per Diem Plus, LLC. The Per Diem Plus logo and Per Diem Plus are trademarks of Per Diem Plus, LLC.

Per Diem Plus launches enhancements to its automated per diem and expense tracking Android app for truck drivers

5/13/2016

ST. LOUIS — Per Diem Plus, LLC, the first ever automated per diem and expense tracking Android app for truck drivers, today announced the launch of several enhancements. Per Diem Plus is designed to streamline and eliminate the guesswork out of taxrelated recording keeping for drivers who deduct travel and business expenses on their own tax returns.

“We encourage feedback from the drivers using Per Diem Plus and the enhancements we recently launched are a direct result of their valuable input” said John Stefek, Director of Client Experience.

Enhancements to the Per Diem Plus app include:

An Apple iOS version of Per Diem Plus is currently in development and scheduled for release in the late summer of 2016.

Please visit www.perdiemplus.com for more information including a step-by-step demonstration of how Per Diem Plus works.

Per Diem Plus was developed and is managed in the USA by tax professionals with experience in the transportation industry. For more information or to schedule an interview with one of our tax experts, please contact John Stefek at johns@perdiemplus.com or 3144096454.