At Per Diem Plus, we believe customers deserve to understand our policies for responding to government requests for their data. In addition to the detailed frequently asked questions (FAQs) below, there are some core policies we adhere to across our services:

Per Diem Plus does not provide any government with direct and unfettered access to our customers’ data.

If a government wants customer data, it must follow applicable legal process. It must serve us with a warrant or court order for content, or a subpoena for subscriber information or other data.

All requests must target specific accounts and identifiers.

Per Diem Plus reviews all requests to ensure they are valid, rejects those that are not valid, and only provides the data specified.

Q: What is the process for disclosing customer information in response to government legal demands?

A: Per Diem Plus requires an official, signed document issued pursuant to local law and rules. Specifically, we require a subpoena or equivalent before disclosing data, and only disclose content to law enforcement in response to a warrant (or its local equivalent). Per Diem Plus reviews government demands for customer data to ensure the requests are valid, rejects those that are not valid, and only provides the data specified in the legal order.

Q: Is rejecting a request the only way Per Diem Plus resists government requests?

A: No. We may seek to narrow the scope of requests. When a request addresses our commercial services, we always attempt to redirect the government to obtain the information directly from our customer. Except in the most limited circumstances, we believe that government agencies can go directly to business customers for per diem data information about one of their employees and that they can do so without undermining their investigation. If needed, we may also file a formal legal challenge in court seeking to modify or quash a legal order.

Q: Does Per Diem Plus provide any data to governments absent a formal legal request?

No.

Q: Does Per Diem Plus notify users of its consumer services, such as Per Diem Plus – Owner Operators, when law enforcement or another governmental entity in the U.S. requests their data?

A: Yes. Per Diem Plus gives prior notice to users whose data is sought by a law enforcement agency or other governmental entity, except where prohibited by law. We may withhold notice in exceptional circumstances, such as emergencies where notice could result in danger, or where notice would be counterproductive (e.g., where the user’s account has been hacked). Per Diem Plus also provides delayed notice to users upon expiration of a valid and applicable nondisclosure order unless Per Diem Plus, in its sole discretion, believes that providing notice could result in danger to identifiable individuals or groups or be counterproductive.

Q: Does Per Diem Plus notify its enterprise customers when law enforcement or another governmental entity requests their data?

A: Yes. Per Diem Plus gives prior notice to its enterprise customers of any third-party requests for their data, except where prohibited by law. We also provide our enterprise customers with notice upon expiration of a valid and applicable nondisclosure order. Except in the most limited circumstances, we believe governments can obtain information directly from our enterprise customers without jeopardizing investigations. For the same reason, we believe that our enterprise customers can, except in the most exceptional circumstances, be notified about government requests for their data.

Q: Does Per Diem Plus disclose additional data as a result of the CLOUD Act?

A: No. The CLOUD Act amends U.S. law to make clear that law enforcement may compel U.S.-based service providers to disclose data that is in their “possession, custody, or control” regardless of where the data is located. This law, however, does not change any of the legal and privacy protections that previously applied to law enforcement requests for data – and those protections continue to apply. Per Diem Plus adheres to the same principles and customer commitments related to government demands for user data.

Q: Does Per Diem Plus provide customer data in response to legal demands from civil litigation parties?

A: Per Diem Plus may receive legal demands for customer data from civil litigation. Per Diem Plus does not respond to private requests other than those received through a valid legal process. Per Diem Plus adheres to the same principles for all requests from civil proceeding legal requests as it does for government agencies requests for user data, requiring nongovernmental civil litigants to follow the applicable laws, rules and procedures for requesting customer data.

If a nongovernmental party wants customer data, it needs to follow applicable legal process — meaning, it must serve us with a valid subpoena or court order for content or subscriber information or other noncontent data. For content requests, we require specific lawful consent of the account owner and for all requests we provide notice to the account owner unless prohibited by law from doing so. We require that any requests be targeted at specific accounts and identifiers. Per Diem Plus’s reviews civil proceeding legal requests for user data to ensure the requests are valid, rejects those that are not valid, and only provides the data specified in the legal order.

If you have any questions, concerns or comments regarding this Policy or any other security concern, contact us at: Per Diem Plus, LLC, 8924 E Pinnacle Peak Rd, G5-452, Scottsdale, AZ 85295 or by telephone at 314-488-1818.

Copyright 2022 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.®

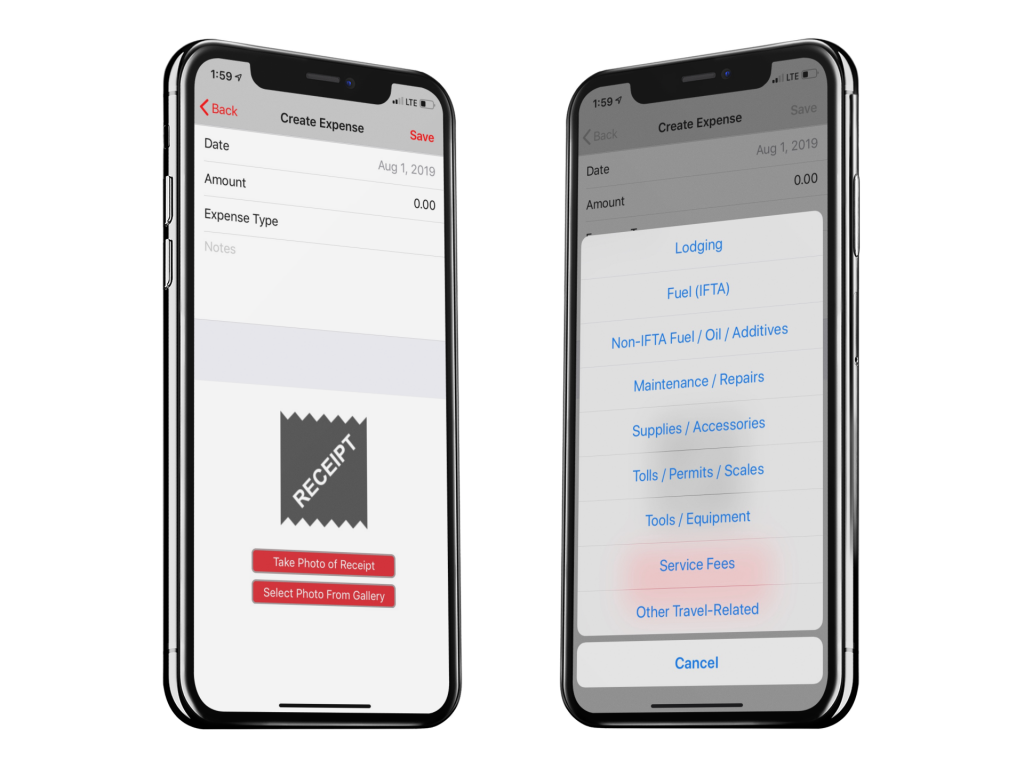

Per Diem Plus was designed by tax pro's to make trucker expense tracking easy! Follow these simple steps to record your first expense:

Select the EXPENSES tab

ANDROID: Tap the "Add Expenses" button; iOS: Tap the "+" sign upper righthand corner of the screen

Choose the Date

Enter the dollar amount of the expense

Select the Expense Type from the list

Select "Take Photo of Receipt" or select a photo from your gallery

Tap SAVE to record the expense

Tip 1: Receipts images are stored on the PDP cloud servers for 4 years

Tip 2: You can delete receipt photos after saving an expense to free up memory / storage on your device.

Have a tax question? Request a free consultation HERE with Mark W. Sullivan, EA

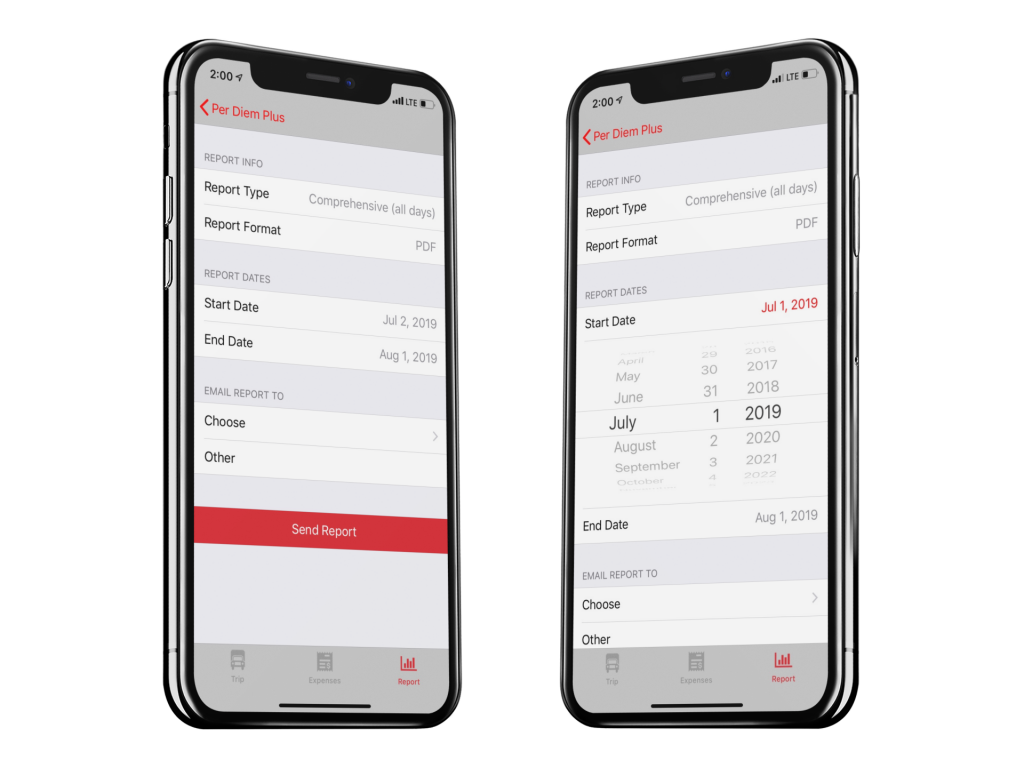

Create an itemized per diem and expense report in the Per Diem Plus app by following these simple steps.

Select REPORT

Choose Report Type - Qualified Per Diem Days or Comprehensive (all days)

Choose a Report Format.

Tip: Only the CSV format includes receipts

Choose the Start and End Date

Choose who to email the report to

Tip: The Other option allows you to enter an email not associated with your account, i.e. your accountant

Tap Send Report

Tip 1: If you scan a lot of receipts the report may exceed your email providers file size permission. Select a shorter start and end date, i.e. run quarterly reports

Tip 2: Check your SPAM / JUNK folder if did not receive the report

Have a tax question? Request a free consultation HERE with Mark W. Sullivan, EA

The Per Diem Plus mobile app was designed by drivers to be easy to use.

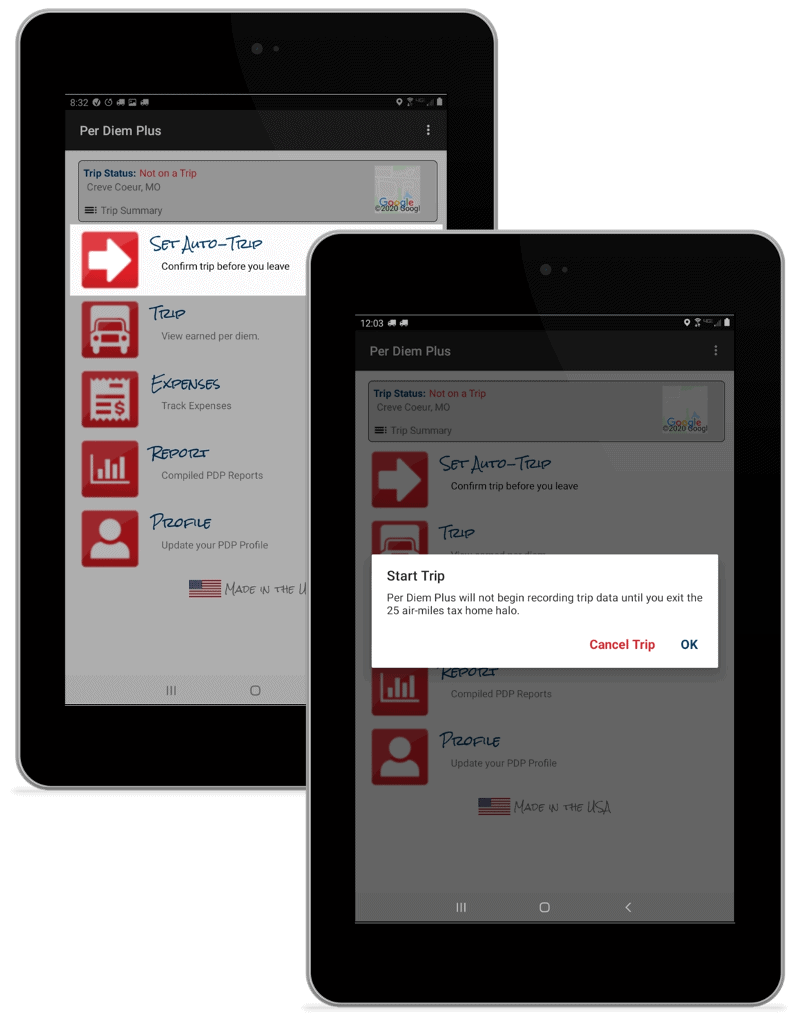

How do I start a trip? Select "Set Auto Trip". The app will begin tracking your trip automatically when you exit the 25 air-miles tax home halo.

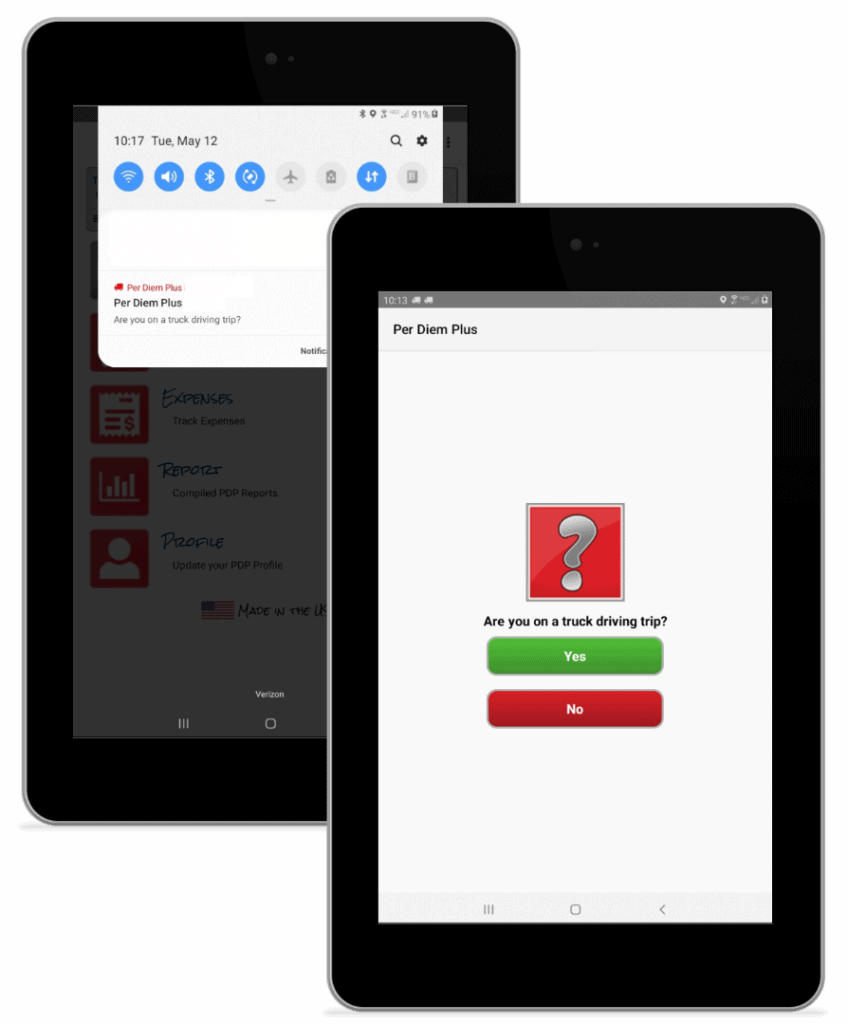

How do I start a trip if I forgot to Set Auto-Trip? The app will post a notification asking if you are on a truck driving trip. Confirm the notification to track per diem for your current trip.

When will I see my per diem? Per diem is recorded the following afternoon and includes 34-hour restarts and unforeseen delays like detention, weather and breakdowns.

How do I end a trip? The app ends a trip automatically when you return to your tax home.

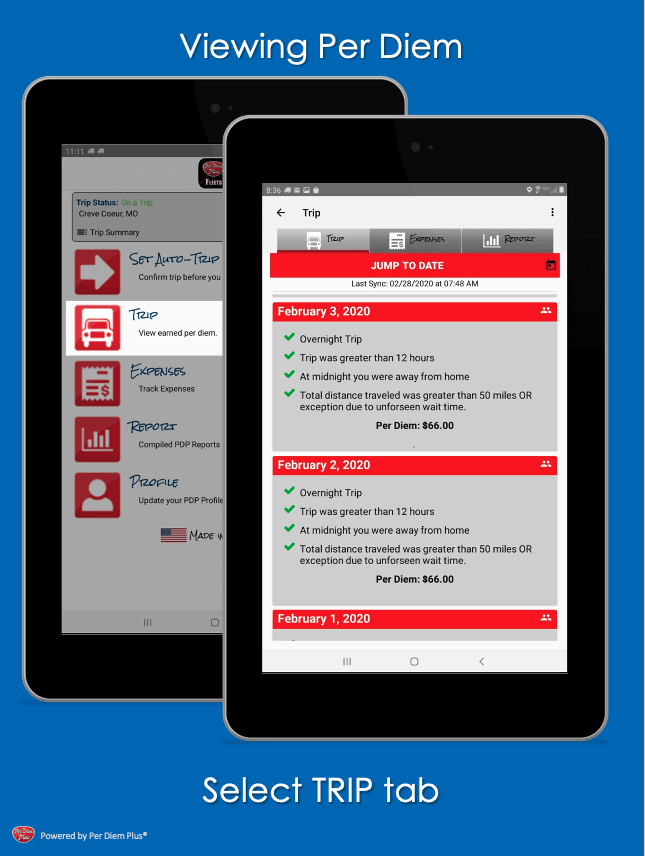

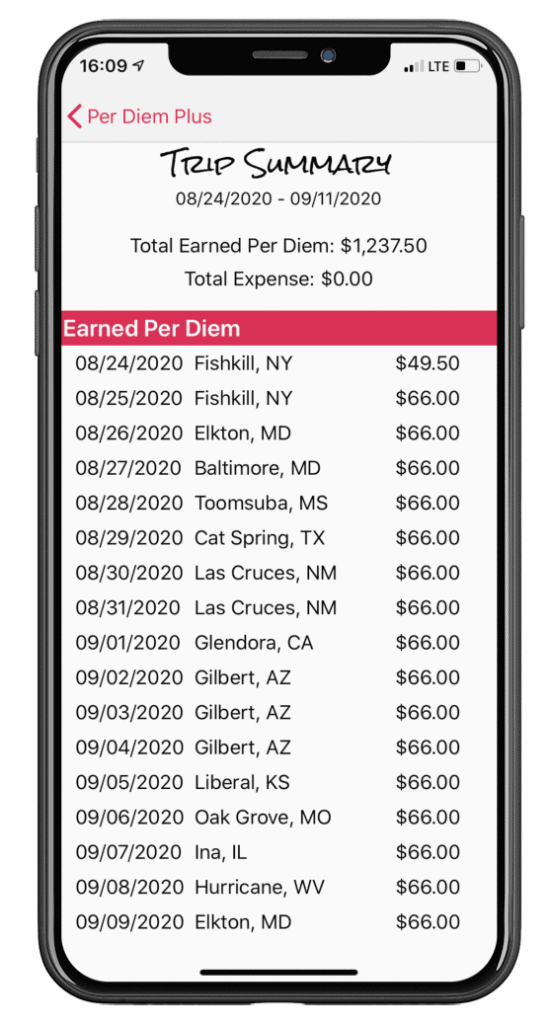

How do I view my per diem? Select the TRIP tab or TRIP SUMMARY.

Use the Trip Summary get a quick snapshot of your driver per diem.

Trip Summary: Features includes an itemized record with IRS-required "date, place and per diem amount" for the current truck driving trip, total expenses and expenses totals summarized by categorized by type.

These feature can be accessed by tapping Trip Summary on the app home screen.

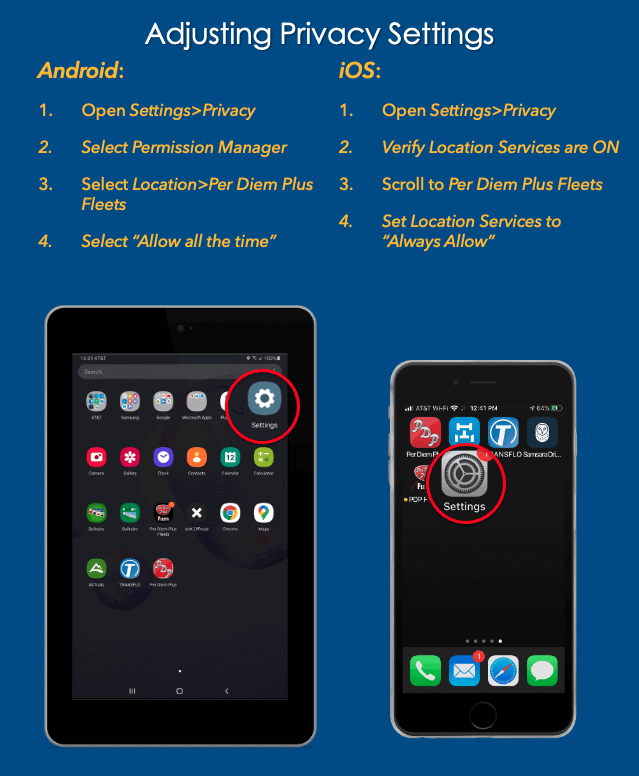

The Per Diem Plus-Owner Operators mobile app requires your location to determine if you qualify for per diem. Both Android and iOS OS may change app privacy settings back to "Only While Using App" without notice. Please confirm Privacy Settings are set to "Always Allow":

Android

Open Settings>Privacy

Select Permission Manager>Location

Select Per Diem Plus>Set to “Allow all the time”

iOS

Open Settings>Privacy

Verify Location Services are ON

Select Per Diem Plus>Select "Always Allow"

Have a tax question? Request a free consultation HERE with Mark W. Sullivan, EA

Here are some tips to insure you maximize your driver per diem with Per Diem Plus.

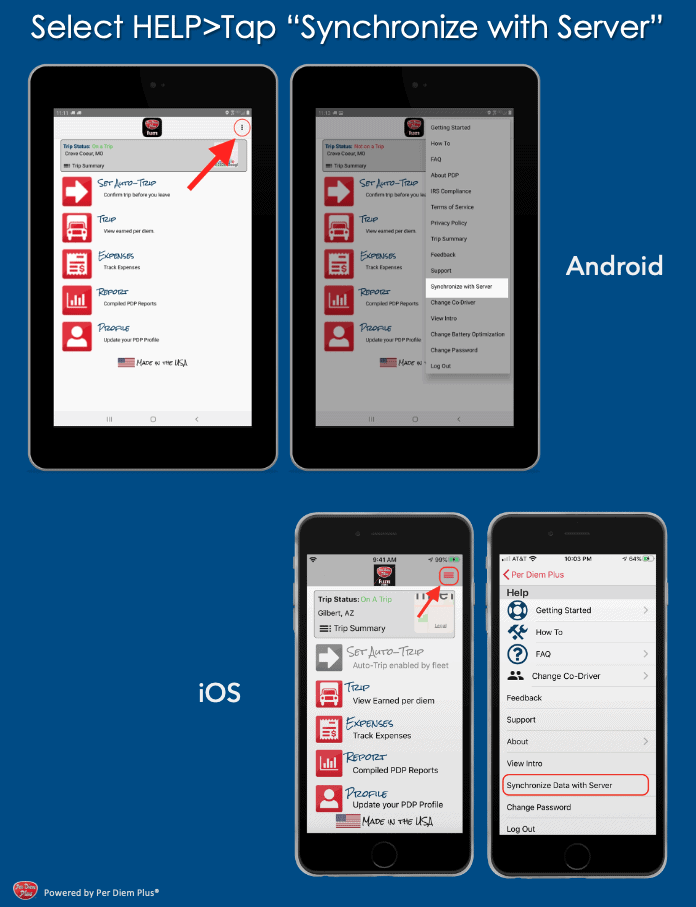

Tip 1: The app attempts to pull trip data hourly while you are on a trip, however, cellular network and connectivity issues may prevent the data from uploading to our cloud servers where per diem is calculated and download back to your device. You can manually push trip data to our servers by selecting "Synchronize with Server" in the HELP menu.

Tip 2: Synchronize your device data weekly

Tip 3: Use the Trip Summary to get a quick snapshot of your driver per diem that includes an itemized record with IRS-required "date, place and per diem amount" for the current truck driving trip, total expenses and expenses totals summarized by categorized by type.

These feature can be accessed by tapping Trip Summary on the app home screen.

Have a tax question? Request a free consultation HERE with Mark W. Sullivan, EA

The Per Diem Plus Owner Operators and Fleets mobile apps require your location to determine if you qualify for per diem. Both Android and iOS OS require you to change app privacy settings "Always Allow" or "Allow all the time". Please confirm Privacy Settings are set correctly:

Android

Open Settings>Privacy

Select Permission Manager>Location

Select Per Diem Plus Fleets>Set to “Allow all the time”

iOS

Open Settings>Privacy

Verify Location Services are ON

Select PDP Fleets>Select "Always Allow"

Motorola

Swipe up on the device home screen to view your apps