State Income Tax Considerations on Driver Per Diem

2021 TAX LAW UPDATE - READ ABOUT 100% DEDUCTION FOR PER DIEM

No per diem tax analysis would be complete without addressing the state income tax considerations on driver per diem. In our last blog post, No Driver Per Diem Yields Surprise Tax Bill, we showed you an example of a driver not receiving per diem. In this article, we will show you the negative impact of living in a high-tax state.

Johnny Mills is an over-the-road company driver

- Lives with his wife and 3 children in Connecticut - a high-tax state

- Spent 295 nights away from home on the road in 2019

- Averaged 2,700 miles/week, and

- Had a banner year in earnings

- His employer has terminals in 5 other states and uses the Per Diem Plus Fleets mobile app platform to administer their per diem plan

Since, Johnny elected not to enroll in the employer plan when he joined the company, he paid an extra $7,064 in federal income and payroll taxes. But how much extra state income tax did he pay? Would it make financial sense for him to move his family and transfer to one of the company's other terminals, like nearby Arizona?

High-Tax vs Low-Tax State Income Tax Considerations

No discussion on the benefits of per diem for truck drivers would be complete without considering state income taxes. State income taxes substantially impact a driver's overall income tax burden. Drivers in high-tax states like California, Connecticut or New York should consider the state tax savings of per diem. These savings are even more pronounced when compared to low-tax states like Arizona.

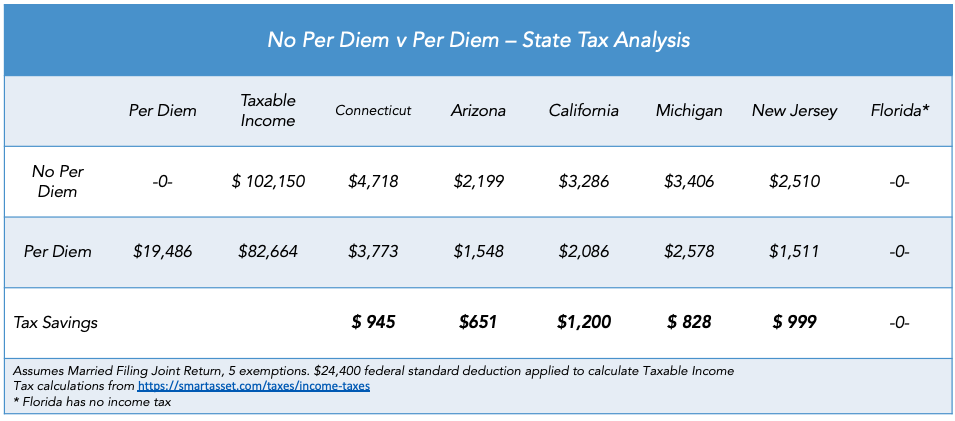

State Tax Savings: Enrolling in the company per diem plan would have saved Johnny $ 945 in Connecticut income tax for 2019.

State vs State Analysis: A Connecticut driver paid $4,718 of state income tax in 2019. An identical Arizona-based driver paid only $2,199 - a $2,519 difference.

State Tax Implications - No Per Diem vs. Per Diem

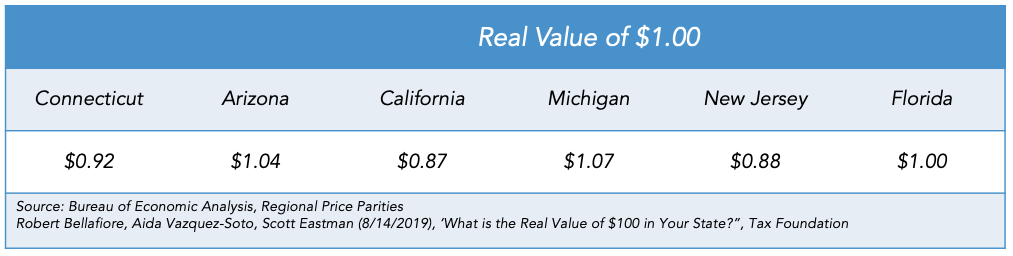

The Real Value of $1.00

The real value of a dollar (purchasing value) must be taken into consideration in order to make state-to-state comparisons. For example, $1.00 is only worth $0.92 cents in Connecticut but $1.04 in Arizona - a 11.5% difference.

- The real dollar value reduces the $ 954 Connecticut tax savings to $ 836, meanwhile the $651 Arizona tax savings increase to $677.

- Living in Connecticut reduced the value of Johnny's 2019 income of $126,550 by nearly 9% or $11,136.

- If he lived in Arizona $126,550 of income increases by $5,062 of real dollar value to $131,612.

- Johnny would realize about $16,198 in real value benefit by moving to a low-cost, low-tax state like Arizona from Connecticut.

Conclusion

No per diem tax analysis would be complete without addressing the state income tax considerations on driver per diem. Johnny Mills received an unpleasant surprise this tax season because he did not participate in his employer offered per diem plan - an additional $7,064 of federal and $ 945 in state income taxes. Living in high-cost, high-tax Connecticut further reduced the value of his earnings by over $11,136. However, if Johnny enrolls in the company per diem plan and moves his family to a low-cost, low-tax state like Arizona it would generate about $16,198 in real dollar value.

About Per Diem Plus FLEETS

Per Diem Plus FLEETS is a proprietary mobile software application that was designed by truckers and built by tax pros. It is the only IRS-compliant mobile app for iOS and Android that automatically tracks each qualifying day of travel in the USA & Canada and replaces ELD backups (logbooks) to substantiate away-from-home travel.

This article was written by Mark W. Sullivan EA, Tax Counsel for Per Diem Plus, who has over a decade of experience advising trucking companies on per diem issues. Prior to starting a private practice in 1998, Mr. Sullivan was an Internal Revenue Officer with the New York, NY, Saint Louis, MO and Washington, D.C. offices of the Internal Revenue Service. Questions? Contact Mark W. Sullivan, EA.

Copyright 2020 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.®

Disclaimer: This article is for information purposes only and cannot be cited as precedent or relied upon in a tax dispute before the IRS.

Reference:

https://taxfoundation.org/real-value-100-state-2019/

https://taxfoundation.org/state-individual-income-tax-rates-and-brackets-for-2020/