PDP For Fleets - 3 Months Free

Pros & Cons: Schedule C vs S-Corp for Self-Employed Truckers is from "Making The IRS Work In Your Favor" presented by Mark W. Sullivan, EA at the CMC LIVE hosted by Kevin Rutherford and Let's Truck.

IRS Orders Immediate Stop To New Employee Retention Credit Claims (IRS Newswire, 9/14/23)

IRS Issues 2024 Trucker Per Diem Rates (9/25/23)

Pros & Cons: Schedule C vs S-Corp for Self-Employed Truckers general rule of thumb:

It is important to note that entity classifications like Limited Liability Company (LLC) and Limited Liability Partnership (LLP) are a function of state law and not federal. For federal purposes the entity type is a tax election.

What qualifies as "reasonable wages" has been a matter of debate for more than 100 years. However, in trucking a safe-haven would be to pay yourself a wage equal to that which an employee truck driver would be paid for doing the same job. Hint: Paying yourself $20,000 of wages as an OTR driver clocking 110,000 miles annually and $80,000 of draw would likely be classified as unreasonable.

The procedures for compensating yourself for your efforts in carrying on a trade or business will depend on the type of business structure you elect. Below are topics that frequently arise when new business owners ask the Internal Revenue Service questions about paying themselves.

An officer of a corporation is generally an employee. However, an officer who performs no services or only minor services and who neither receives nor is entitled to receive any pay is not considered an employee. Refer to "Who Are Employees?" in Publication 15-A, Employer's Supplemental Tax Guide.

Partners are not employees and should not be issued a Form W-2, Wage and Tax Statement, in lieu of Form 1065, Schedule K-1, for distributions or guaranteed payments from the partnership. Refer to Tax Information for Partnerships page for more information.

Any distribution to shareholders from earnings and profits is generally a dividend. However, a distribution is not a taxable dividend if it is a return of capital to the shareholder. Most distributions are in money, but they may also be in stock or other property. For information on shareholder reporting of dividends and other distributions, refer to Publication 550, Investment Income and Expenses.

You cannot designate a worker, including yourself, as an employee or independent contractor solely by the issuance of Form W-2, Wage and Tax Statement or Form 1099-NEC, Nonemployee Compensation. It does not matter whether the person works full time or part time. You use Form 1099-NEC to report payments to others who are not your employees. You use Form W-2 to report wages, car allowance, and other compensation for employees.

You will be liable for social security and Medicare taxes and withheld income tax if you do not deduct and withhold them because you treat an employee as a nonemployee, including yourself if you are a corporate officer, and you may be liable for a trust fund recovery penalty. Refer to Publication 15, Circular E, Employer's Tax Guide for details about the trust fund recovery penalty or Independent Contractor (Self-Employed) or Employee? for more information on employee classification.

A loan by a corporation to a corporate officer should include the characteristics of a loan made at arm's length. That is, there should be a contract with a stated interest rate, a specified length of time for repayment, and a consequence for failure to repay the loan. Collateral would also be an indication of a loan. A below-market loan is a loan which provides for no interest or interest at a rate below the federal rate that applies. If a corporation issues you, as a shareholder or an employee, a below-market loan, then depending on the substance of the transaction the lender's payment to the borrower is treated as a gift, dividend, contribution to capital, payment of wages, or other payment.

See "Below-market interest rate loans" under Employees' Pay / Kinds of Pay / Loans or Advances in Publication 535, Business Expenses for more information.

Because an officer of a corporation is generally an employee with wages subject to withholding, corporate officers may question what is considered reasonable compensation for the efforts they contribute to conducting their trade or business. Wages paid to you as an officer of a corporation should generally be commensurate with your duties. Refer to "Employee's Pay, Tests for Deducting Pay" in Publication 535, Business Expenses for more information. Public libraries may have reference sources that provide averages of compensation paid for various types of services. The Internal Revenue Service may determine that adjustments must be made to the income and expenses of tax returns for both the corporation and an individual shareholder if the officer is underpaid for services provided.

Per Diem Plus Small Fleets requires users to complete the account setup HERE before using the app.

Per Diem Plus Fleets is also available on the Truckstop Marketplace, Samsara App Marketplace and Platform Science Marketplace

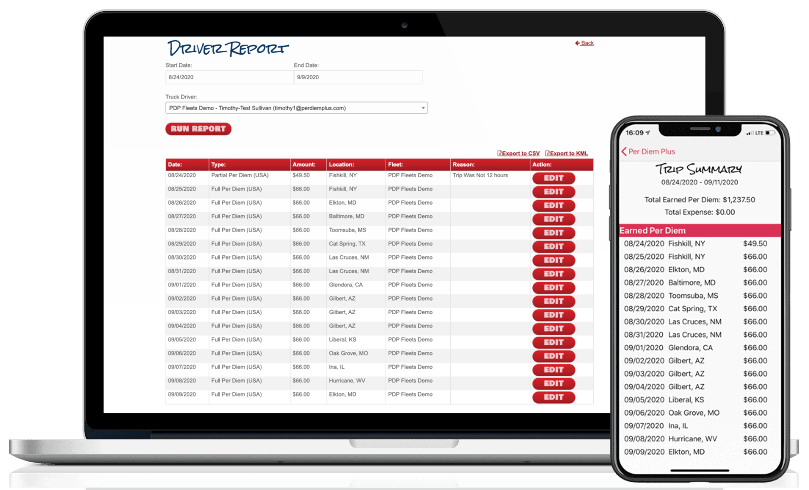

Per Diem Plus is a proprietary mobile software application that was designed by truckers and built by tax pros. It is the only IRS-compliant mobile app for iOS and Android that automatically tracks each qualifying day of travel in the USA & Canada and replaces ELD backups (logbooks) to substantiate away-from-home travel.

Mark is tax counsel for Per Diem Plus. With nearly two decades of experience advising trucking companies on per diem issues, Mark was responsible for defining the Per Diem Plus software logic rules that automatically calculates trucker per diem in accordance with IRS regulations. He also previously served as the consulting per diem tax expert for Omnitracs.

In addition to his time working with Per Diem Plus, Mark works in private practice as an Enrolled Agent at Mark Sullivan Consulting, PLLC specializing in federal tax controversy representation and consulting. He also served as the consulting and expert witness for the Federal Defenders Office and private defense counsel in financial crimes cases in multiple federal district courts. Contact Mark W. Sullivan, EA

Disclaimer: This article includes general tax information, and therefore may not be relied upon as legal authority. This means that the information cannot be used to support a legal argument in a court case. Please consult with a licensed tax professional.

Copyright 2020-2023 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.®

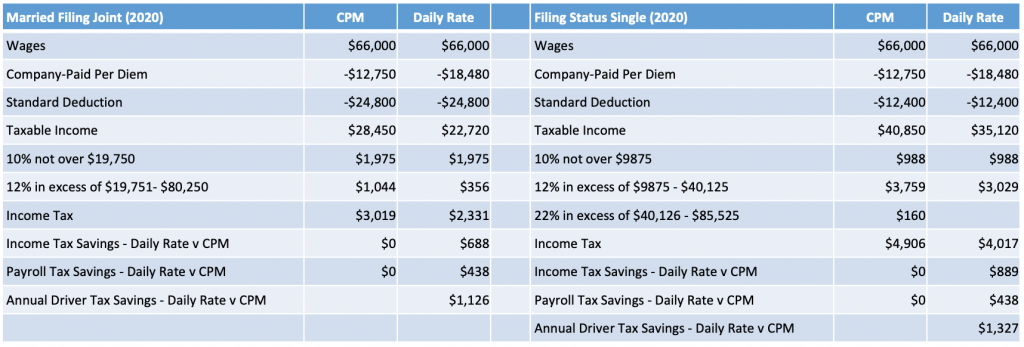

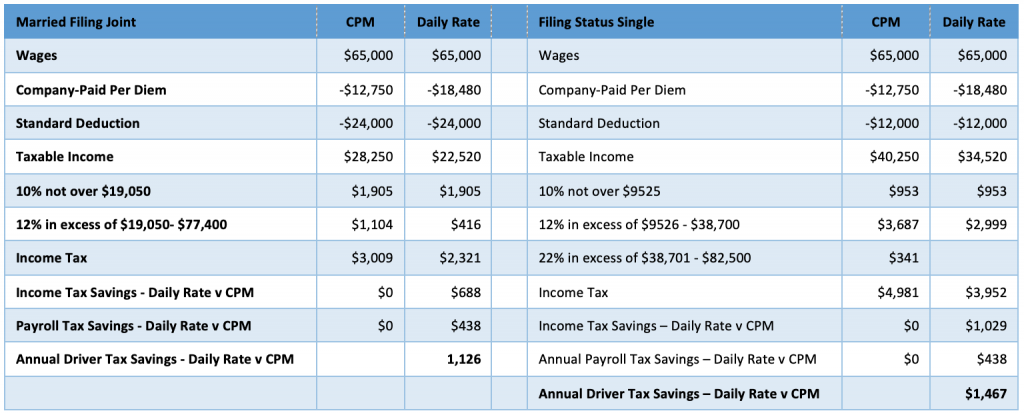

Substantiated per diem provides the largest benefit to both a driver and fleet over the old cent-per-mile method. Decades before the advent of TMS software, telematics and ELD's fleets adopted cent-per-mile per diem. Why? Because it was easy to calculate and substantiate using trip sheets[i]. However, there is no correlation between the miles a driver travels and frequency of meal breaks.

Under the cent-per-mile method a driver is paid only for miles driven and not nights away from home. Although, a driver may travel 500 miles one day they may only clock 200 miles the next. In the end, the distance traveled does not affect the need to eat 3 meals a day.

The IRS introduced the Special Transportation Industry substantiated per diem to simplify tax compliance for fleets by relying on days away from home instead of miles traveled. This method accurately reflects the number of meals a driver eats and resolved the problem that driver’s regularly travel away from home and stop during a single trip at localities with differing federal M&IE rates.

Use our Fleet Per Diem Benefit Calculator to learn how much your fleet can save with Per Diem Plus Fleets.

[i] 1-274-5T(c) Rules of substantiation, Rev. Proc. 2011-47 § 4.02(5)

Both the substantiated and cent-per-mile per diem methods are IRS-compliant. However, a motor carrier that adopts the substantiated per diem method that is built into Per Diem Plus FLEETS will realize the most benefit for both the fleet and their drivers.

Per Diem Plus FLEETS is a configurable mobile application enterprise platform that automates administration of an IRS-compliant accountable per diem plan for truck drivers and fleets managers. No matter how big or small your company is, Per Diem Plus has a solution for you.

Per Diem Plus FLEETS is a proprietary mobile software application that was designed by truckers and built by tax pros. It is the only IRS-compliant mobile app for iOS and Android that automatically tracks each qualifying day of travel in the USA & Canada and replaces ELD backups (logbooks) to substantiate away-from-home travel.

This article was written by Mark W. Sullivan EA, Tax Counsel for Per Diem Plus, who has over a decade of experience advising trucking companies on per diem issues. Prior to starting a private practice in 1998, Mr. Sullivan was an Internal Revenue Officer with the New York, NY, Saint Louis, MO and Washington, D.C. offices of the Internal Revenue Service.

Questions? Contact Mark W. Sullivan, EA.

Disclaimer: This article is for information purposes only and cannot be cited as precedence or relied upon in a tax dispute before the IRS.

Copyright 2019-2022 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.®

Which per diem method saves a fleet more money? Substantiated per diem saves a motor carrier the most money, since the fleet benefits are directly proportional to total per diem paid to drivers. So how did cent-per-mile per diem become so popular in the trucking industry? Decades before the advent of telematics fleets adopted cent-per-mile per diem for because it was easy to calculate. However, there is no correlation between the miles a driver travels and meal breaks.

Drivers prefer substantiated special trucker per diem. Why? They eat 3 meals a day regardless of whether they drive 200 or 600 miles. The IRS introduced the Special Transportation Industry substantiated per diem to remedy this issue. In addition it simplified tax compliance for fleets by relying on nights away from home instead of miles traveled. It is also a more accurate reflection of anticipated meal expenses for drivers.

Use our Fleet Per Diem Benefit Calculator to learn how much your fleet can save with Per Diem Plus Fleets.

Adding an accountable per diem program for employee drivers is a sure-fire way to enhance driver recruiting and retention. Consider the following:

Both substantiated and cent-per-mile per diem must comply with the IRS substantiation by adequate records rules. According to the IRS, "a motor carrier must maintain lrecords to establish "time, place and location" for each per diem event". The Per Diem Plus FLEETS platform satisfies this requirement since it is maintained in such manner that each recording of an element of an expenditure is made at or near the time of the expenditure.

Document retention rules:

The transportation industry has been unique in its treatment of driver per diem for over 30 years. The substantiated per diem method saves a motor carrier more money than cent-per-mile method. While, substantiated and cent-per-mile per diem methods are IRS-compliant, both require a motor carrier to comply with the adequate records and document retention rules.

Per Diem Plus FLEETS is a configurable mobile application enterprise platform that automates administration of an IRS-compliant accountable per diem plan for truck drivers and fleets managers. No matter how big or small your company is, Per Diem Plus has a solution for you.

Per Diem Plus FLEETS is a proprietary mobile software application that was designed by truckers and built by tax pros. It is the only IRS-compliant mobile app for iOS and Android that automatically tracks each qualifying day of travel in the USA & Canada and replaces ELD backups to substantiate away-from-home travel.

This article was written by Mark W. Sullivan EA, Tax Counsel for Per Diem Plus, who has over a decade of experience advising trucking companies on per diem issues. Prior to starting a private practice in 1998, Mr. Sullivan was an Internal Revenue Officer with the New York, NY, Saint Louis, MO and Washington, D.C. offices of the Internal Revenue Service. Questions? Contact Mark W. Sullivan, EA.

Copyright 2019-2022 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.®

Disclaimer: This article is for information purposes only and cannot be cited as precedence or relied upon in a tax dispute before the IRS.

The following excerpt on the home office deduction is from "Making The IRS Work In Your Favor" presented by Mark W. Sullivan, EA at the 2018 CMC LIVE hosted by Kevin Rutherford and Let's Truck.

Taxpayers are not entitled to claim the home office deduction unless the expenses are attributable to a portion of the home, or a separate structure, used exclusively on a regular basis for business purposes. Here is what you need to know to take advantage of a great tax saving opportunity.

Only self-employed individuals may claim the home office deduction.

Portion of home used exclusively

(Refer to IRC Sec 280A(a), 280A(c), 280A(c)(1)(A))

(Refer to IRC Sec 280A(c)(5)(A))

PDP Small Fleets requires users to complete the account setup HERE before using the app.

Mark is tax counsel for Per Diem Plus. With nearly two decades of experience advising trucking companies on per diem issues, Mark was responsible for defining the Per Diem Plus software logic rules that automatically calculates trucker per diem in accordance with IRS regulations. He also previously served as the consulting per diem tax expert for Omnitracs.

In addition to his time working with Per Diem Plus, Mark works in private practice as an Enrolled Agent at Mark Sullivan Consulting, PLLC specializing in federal tax controversy representation and consulting. He also served as the consulting and expert witness for the Federal Defenders Office and private defense counsel in financial crimes cases in multiple federal district courts. Contact Mark W. Sullivan, EA

Disclaimer: This article is for information purposes only and cannot be cited as precedent or relied upon in a tax dispute before the IRS.

Copyright 2018-2023 Mark Sullivan Consulting, PLLC; Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.®

The following excerpt, "Paying your kids", is from "Making The IRS Work In Your Favor" presented by Mark W. Sullivan, EA at the 2018 CMC LIVE hosted by Kevin Rutherford and Let's Truck.

Trucking like any small business is often a family affair. My son started working in my accounting practice after school when he was 10 - shredding paper, stamping and stuffing envelopes. Whether you are a solo owner operator or run a trucking company, it is not uncommon to put your kids to work helping in the business. Here is what you need to know to take advantage of a great tax saving opportunity.

First and foremost: Your children must be bona fide employees

WARNING:

Sole Proprietorship / Partnerships

Children under 21 wages subject to income tax withholding, but not :

Corporations

Children under 21 are subject to:

In 2018 the standard deduction for SINGLE filers raised from $6,350 to $12,000.

|

Example: Employment Tax on Wages of $12,000 |

||

|

Sole-Proprietor |

Corporation |

|

| FICA / Medicare / FUTA 16.8% | $0.00 |

$2,016 |

Reference Material:

Refer to: https://www.irs.gov/businesses/small-businesses-self-employed/family-help

Start your 30-day FREE trial with no credit card required today!

Per Diem Plus is a proprietary mobile software application that was designed by truckers and built by tax pros. It is the only IRS-compliant mobile app that automatically tracks each qualifying day of travel in the USA & Canada and replaces ELD backups (logbooks) to substantiate away-from-home travel.

Mark is tax counsel for Per Diem Plus. With nearly two decades of experience advising trucking companies on per diem issues, Mark was responsible for defining the Per Diem Plus software logic rules that automatically calculates trucker per diem in accordance with IRS regulations. He also previously served as the consulting per diem tax expert for Omnitracs.

In addition to his time working with Per Diem Plus, Mark works in private practice as an Enrolled Agent at Mark Sullivan Consulting, PLLC specializing in federal tax controversy representation and consulting. He also served as the consulting and expert witness for the Federal Defenders Office and private defense counsel in financial crimes cases in multiple federal district courts. Contact Mark W. Sullivan, EA

Disclaimer

This article includes general tax information, and therefore may not be relied upon as legal authority. This means that the information cannot be used to support a legal argument in a court case. Please consult with a licensed tax professional.

If H.R. 1 “Tax Cuts and Job Act” becomes law OTR employee truck drivers will no longer be allowed a tax deduction for unreimbursed business expense, which includes “meal expenses that take place during or incident to any period subject to the Department of Transportation's “hours of service” limits”[i]. As a result, drivers will be required to choose between participating in company-paid per diem plan or cover the cost of their travel-related expenses from after-tax income. Unfortunately, Congress’s “one size fits all” approach overlooked a significant fact: The trucking industry is unique in that it does not utilize the well-established business practice of truly reimbursing for travel-related and other business expenses of employee drivers[ii]. Will Congress now require trucking companies to overhaul their per diem programs to follow business norms?

For over 30 years fleets have utilized a unique reimbursement method for drivers whereby traveled-related expenses (i.e. meals) are deducted from a driver’s gross wages, reclassified as a pre-tax deduction and then added back into wages as non-taxable “per diem” reimbursement – all without changing the gross pay of the driver[iii]. The attractiveness of this per diem method is obvious: At $0.10 CPM a fleet can artificially boost driver take home pay by $40/week or $0.017 CPM without raising labor costs.

For over 30 years fleets have utilized a unique reimbursement method for drivers whereby traveled-related expenses (i.e. meals) are deducted from a driver’s gross wages, reclassified as a pre-tax deduction and then added back into wages as non-taxable “per diem” reimbursement – all without changing the gross pay of the driver[iii]. The attractiveness of this per diem method is obvious: At $0.10 CPM a fleet can artificially boost driver take home pay by $40/week or $0.017 CPM without raising labor costs.

What if a fleet uses the IRS’ Special Transportation Industry rate? At $63 per day a fleet can add $47/week or $0.02 CPM to driver take home pay without raising labor costs.

This article was written by Mark W. Sullivan, EA, who has been providing taxpayer advocacy, consulting, and litigation services since 1998. Prior to starting a private practice Mr. Sullivan was a Revenue Officer with the Internal Revenue Service in New York, NY, St. Louis, MO and Washington, DC. He has over a decade of experience advising transportation industry clients in per diem issues.

Please remember that everyone’s financial situation is different. This article does not give and is not intended to give specific accounting and/or tax advice. Please consult your own tax or accounting professional.

Copyright 2017 Per Diem Plus, LLC. Per Diem Plus proprietary software is the trademark of Per Diem Plus, LLC.

[i] See Internal Revenue Service Notice 2016-58

[ii] Cents-per-mile is the prevailing trucking industry method for calculating company-paid per diem. Drivers subject to DOT Hours of Service regulations are prohibited from using this method.

[iii] Drivers who declined company-paid per diem had the option to claim unreimbursed business expenses at the end of the year as an itemized deduction on Schedule A.